What Happens to the Family Home During Divorce?

If you are going through a divorce, few decisions feel bigger than deciding what happens to the family home.

For many people, the house is more than a financial asset. It is where your children learned to ride their bikes, where birthdays were celebrated, and where daily routines became part of family life.

That is why housing decisions during divorce can feel overwhelming.

You may be asking whether you can afford to keep the house, whether you should sell it, what happens to the mortgage, whether you can buy out your spouse, and how the decision will affect your children.

The goal is not to make the fastest decision. The goal is to make the right decision for your future.

Quick Answer: What Happens to the Family Home During Divorce?

In most divorces, there are four common outcomes for the family home:

- One spouse keeps the home.

- The home is sold and the proceeds are divided.

- One spouse buys out the other spouse’s interest.

- The spouses agree to delay a sale until a future date.

The right option depends on home equity, mortgage obligations, post-divorce income, tax consequences, child-related considerations, and long-term affordability.

The Real Decision Is Bigger Than the House

One of the most common mistakes people make during divorce is treating the family home as an isolated decision.

A home that felt comfortable with two incomes may become difficult to maintain with one. A mortgage payment that once seemed manageable may start competing with child-related expenses, retirement savings, emergency funds, healthcare costs, and future financial goals.

The better question is not, “Can I keep the house?” The better question is, “Can I keep the house while still maintaining financial stability?”

Krystle A. Swopes, EA of BMI Tax & Advisory regularly helps clients evaluate the financial consequences of major life changes, including decisions involving real estate, retirement accounts, and taxes.

Why Keeping the House Is Not Always the Cheapest Option

Many people focus primarily on the mortgage payment when evaluating whether they can afford to stay in the home.

But homeownership also includes property taxes, insurance premiums, maintenance expenses, repair costs, utilities, HOA fees, and unexpected emergencies.

A home that appears affordable on paper may create significant financial pressure once these additional costs are considered.

Timing Can Change the Outcome

One of the most overlooked aspects of divorce-related housing decisions is timing.

Tax consequences are one example. IRS Publication 523 explains important rules involving home sale gain exclusions, transfers between spouses, and tax considerations that may apply to divorced or separated homeowners.

Many families focus only on the sale price. They do not always ask whether the sale will create a taxable gain, whether timing affects tax benefits, or whether tax liens or obligations are connected to the property.

Drawing on experience helping families navigate housing transitions, Vicky Royster of The Move Live Love TX Team encourages homeowners to evaluate both the emotional and financial realities of keeping a home after divorce.

The Biggest Mistake People Make With the Family Home During Divorce

The biggest mistake is making a housing decision based primarily on emotion before understanding the financial reality.

The family home often represents security, familiarity, memories, and stability. But decisions made solely from fear, guilt, nostalgia, or uncertainty can create long-term financial challenges.

- The mortgage is more difficult than expected.

- Property taxes continue to rise.

- Repairs cost more than anticipated.

- Refinancing is harder than assumed.

- Keeping the home limits future flexibility.

A home should provide stability. It should not become a source of ongoing financial stress.

What Can Go Wrong When Housing Decisions Are Rushed?

Financial Consequences

A home that was comfortable during the marriage may become too expensive after divorce. Mortgage payments are only one part of the cost. You must also consider property taxes, insurance, utilities, repairs, maintenance, and emergency expenses.

Emotional Consequences

Letting go of the family home can feel like another loss. Often people are not grieving the property itself. They are grieving the future they expected to have there.

Family Consequences

When children are involved, housing decisions feel heavier. Sometimes stability means remaining in the home. Other times stability comes from reducing financial pressure and creating a healthier long-term environment.

Legal Consequences

Housing decisions can affect property division, debt responsibility, refinancing requirements, future financial obligations, and settlement negotiations.

If one spouse keeps the home but cannot refinance the mortgage, both spouses may remain financially connected to the loan. Even if a divorce decree assigns responsibility to one spouse, lenders may still view both borrowers as responsible.

Attorney Lee Wilson of The Wilson Firm PLLC, whose work frequently involves tax law and complex financial matters, often sees how major property decisions intersect with broader financial obligations.

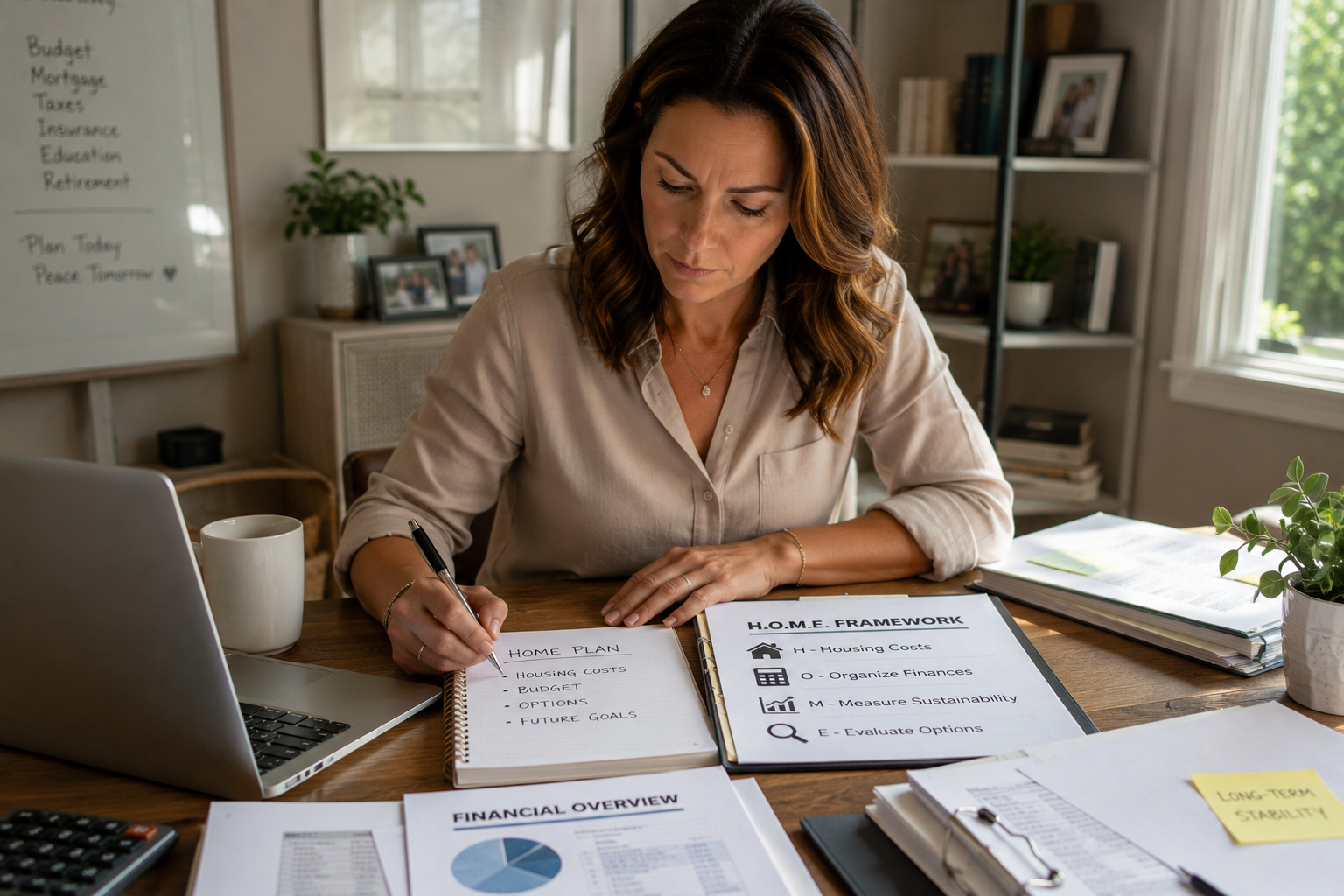

The H.O.M.E. Framework for Better Housing Decisions During Divorce

H — Understand Your Housing Costs

Look beyond the mortgage payment and consider taxes, insurance, utilities, maintenance, repairs, HOA fees, and emergency expenses.

O — Organize Your Financial Picture

Gather your mortgage balance, estimated property value, equity, income after divorce, debt obligations, retirement assets, emergency savings, and future goals.

M — Measure Long-Term Sustainability

Do not only ask whether you can keep the house. Ask whether you can comfortably maintain it one, three, and five years from now.

E — Evaluate Every Available Option

Keeping, selling, buying out a spouse, or delaying a sale may all be reasonable depending on your circumstances.

Understanding Home Equity Before Making a Decision

Before deciding whether to keep or sell the family home, it is important to understand how much equity actually exists.

Home equity is generally the difference between the home’s current market value and the amount still owed on the mortgage.

This information often becomes one of the most important factors when evaluating buyouts, sales, refinancing options, and long-term affordability.

Build a Team That Communicates

Housing decisions during divorce often involve family law attorneys, tax professionals, real estate professionals, mortgage professionals, financial advisors, and title companies.

The key is not simply having professionals involved. The key is making sure they communicate.

Through his work developing professional systems and workflows at Lawgical Workspace, Lee Wilson emphasizes the value of clear communication when multiple professionals are involved in major financial decisions.

Homeowners who need additional housing guidance may benefit from HUD-approved housing counseling resources.

What a Strong Outcome Looks Like

| Strong Decision | Weak Decision |

|---|---|

| Based on affordability | Based on emotion alone |

| Includes tax planning | Ignores future costs |

| Supported by professional guidance | Based on assumptions |

| Focuses on long-term stability | Focuses only on short-term comfort |

Families facing major housing transitions may also benefit from USAGov Housing Help.

Frequently Asked Questions About the Family Home During Divorce

What happens to the family home during divorce?

The home may be sold, one spouse may keep it, or the spouses may create another arrangement as part of the divorce settlement.

Can I keep the house during divorce?

Possibly. The more important question is whether keeping the house remains financially sustainable after the divorce is finalized.

Is selling the house better than keeping it?

There is no universal answer. Selling may create financial flexibility, while keeping the home may provide stability and continuity.

What happens to home equity in a divorce?

Home equity is generally considered part of the property division process. Equity is the difference between the home’s value and the amount owed on the mortgage.

Can one spouse buy out the other spouse’s share?

Yes. A buyout may happen through refinancing, a cash payment, an offset of other marital assets, or another negotiated arrangement.

How does divorce affect the mortgage?

Divorce does not automatically remove someone from a mortgage loan. If both spouses signed the loan, the lender may still consider both responsible unless the mortgage is refinanced, paid off, or otherwise resolved.

What tax issues should I consider before selling the home?

You may need to consider capital gains, home sale exclusions, timing, filing status, and any tax obligations tied to the property. The IRS provides general federal tax resources.

Should I use retirement funds to keep the house?

Be cautious. Retirement accounts may involve taxes, penalties, and long-term financial consequences.

The Best Housing Decision Is the One That Supports Your Future

Many people enter divorce asking, “How do I keep the house?”

A more productive question is, “What housing decision gives me the strongest foundation moving forward?”

Sometimes that answer is keeping the home. Sometimes it is selling the home. Sometimes it involves a buyout, refinancing strategy, or another arrangement entirely.

The right answer depends on your finances, your family, your goals, and the life you want to build after divorce.

Need Help Deciding What Happens to the Family Home?

If you have questions about the family home, property division, or your options during divorce, De Ford Law Firm can help you evaluate your situation and develop a strategy designed to protect your future.

Schedule a Consultation

Recent Comments